Treasury manager

Accounts payable manager

Finance controller

CFO

Payroll manager

Cash management specialist

Compliance officer

Operations director

ACH payment approval is triggered when organizations initiate electronic fund transfers through the ACH network, including vendor payments, payroll disbursements, customer refunds, intercompany transfers, and recurring payments. The process applies when payment amounts exceed automatic processing thresholds, when new payees require validation, when payment details change from established patterns, or when organizational policy mandates dual approval for electronic disbursements. It is critical in organizations with significant payment volumes, those subject to financial controls requirements, and any company where payment fraud risk requires robust authorization procedures.

ACH payment approval typically involves accounts payable or payroll teams who initiate payment requests, finance managers who validate payment details and approve within authority limits, treasury teams who manage bank relationships and transmission, authorized signers who provide final approval for payments exceeding thresholds, and compliance or audit teams who review payment controls. For high-value payments, executive approval may be required.

Reduced payment fraud risk results from validation and dual approval requirements that catch unauthorized or fraudulent payment attempts. Faster payment processing comes from structured approval paths that move legitimate payments through authorization efficiently. Clear payment authorization records provide audit evidence of who approved each disbursement and under what authority. Improved cash management follows from visibility into pending payments and approval status across the payment cycle. Stronger financial controls ensure payments align with organizational policy and regulatory requirements for electronic fund transfers.

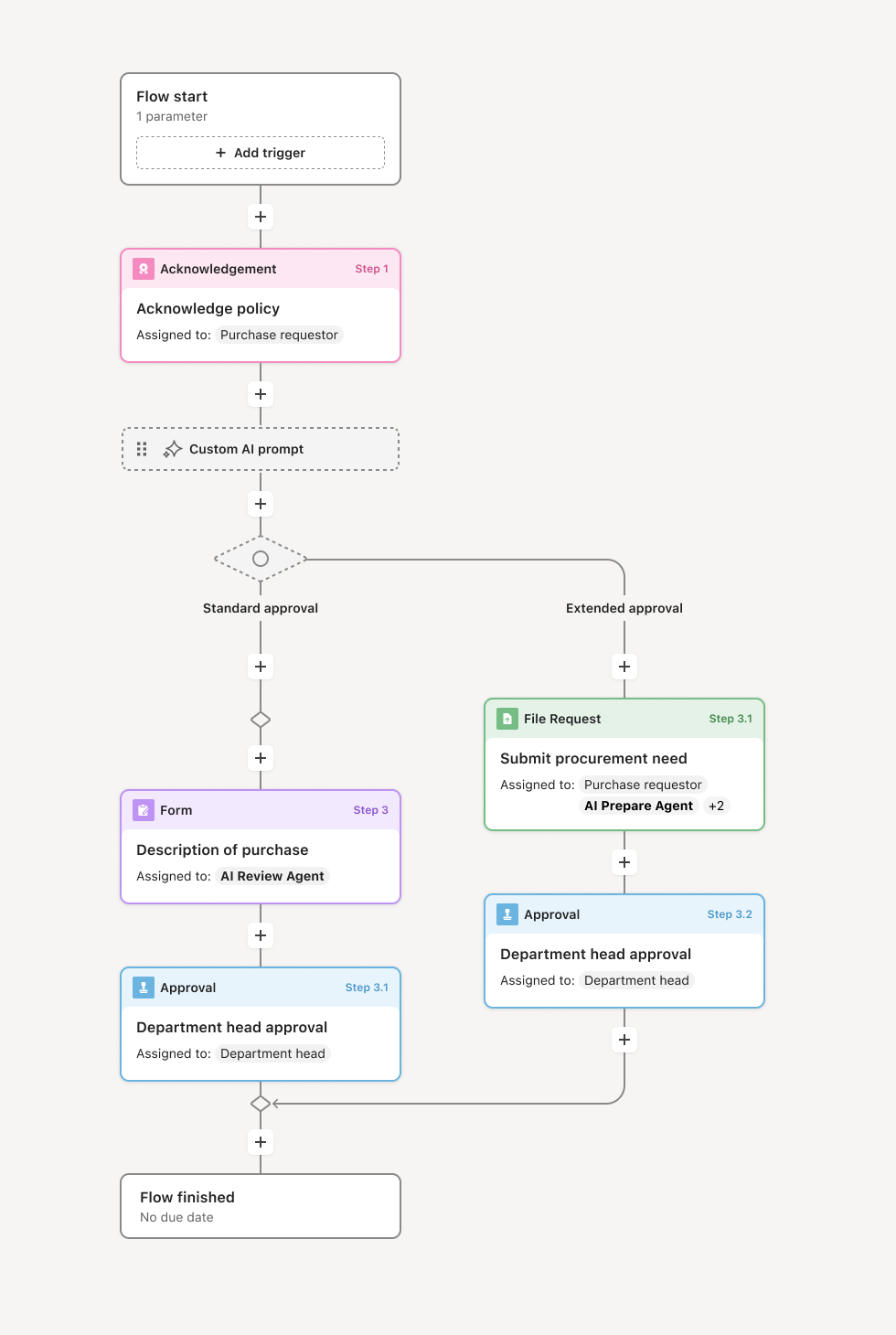

Your version of this process may vary based on roles, systems, data, and approval paths. Moxo's flow builder can be configured with AI agents, conditional branching, dynamic data references, and sophisticated logic to match how your organization runs this workflow. The steps below illustrate one example.

Payment initiation and validation

The process begins when a payment request is submitted, either through accounts payable processing, payroll generation, or manual initiation for ad hoc payments. The request includes payee information, amount, payment date, and supporting documentation such as invoices or payment authorizations. An AI agent may assist by validating payee details against master records, flagging discrepancies, and checking for duplicate payments.

Payee verification

For new payees or changed banking details, additional verification is required before approval. The workflow confirms payee identity and bank account ownership through established verification procedures. Changes to existing payee banking information trigger heightened scrutiny given fraud risk. If verification fails or raises concerns, the workflow routes to treasury or compliance for investigation.

Amount and authority validation

The workflow evaluates the payment amount against approval authority thresholds. Payments within standard limits route to appropriate approvers based on amount and payment type. Payments exceeding thresholds or meeting exception criteria route to senior approvers or require dual authorization. Payroll runs and batch payments may follow dedicated approval paths.

Supporting documentation review

Approvers review the payment request along with supporting documentation to confirm the payment is legitimate and properly authorized. For vendor payments, this includes invoice validation and three-way match confirmation. For payroll, this includes payroll register review. If documentation is incomplete or raises questions, the workflow routes back for clarification before proceeding.

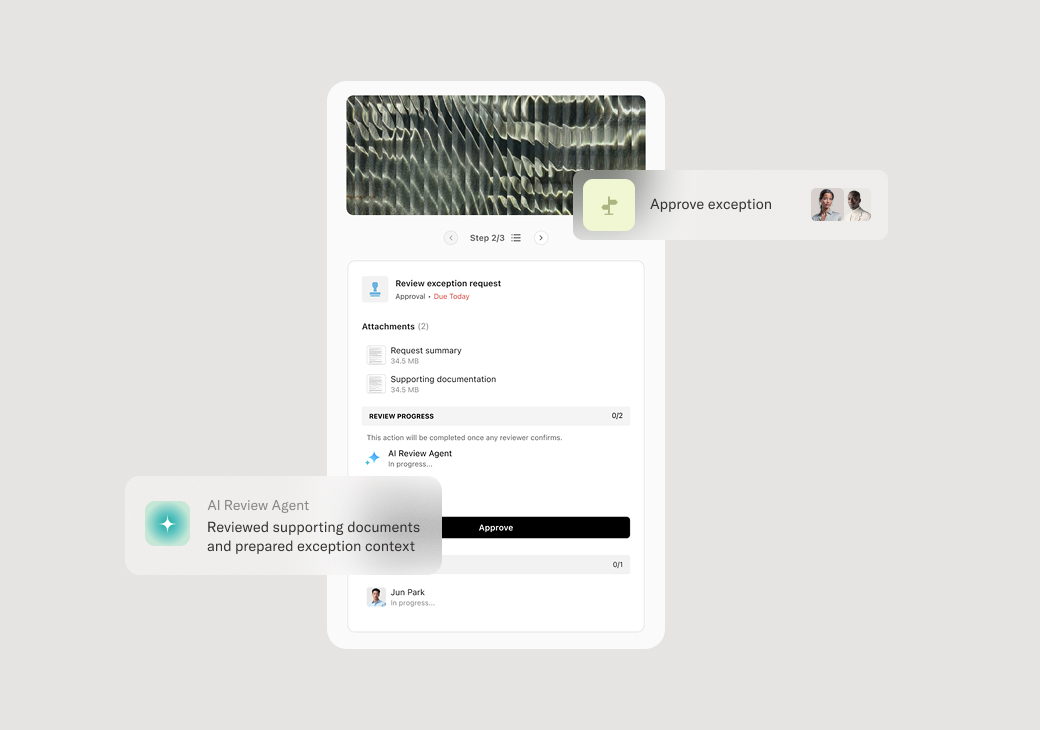

Approval and authorization

Designated approvers formally authorize the payment. Dual approval requirements are enforced where policy mandates. Each approval is captured with the approver's identity, timestamp, and any comments or conditions. If an approver rejects the payment, the workflow captures rejection rationale and notifies the initiator with guidance on next steps.

Transmission and confirmation

Upon final approval, the payment is released for transmission through the ACH network. The workflow tracks transmission status and confirms successful processing. Any transmission failures or returns are flagged for investigation and resolution. The complete payment record including initiation, approval, and transmission is retained.

This process commonly relies on inputs such as payment requests, invoices, payroll registers, payee master data, and bank account verification documentation. It may be triggered by accounts payable batch processing, payroll cycle completion, or manual payment initiation. Supporting systems often include ERP platforms like NetSuite or SAP, treasury management systems, banking platforms, and payroll systems like ADP or Workday.

Key decision points include determining whether payee details require verification, which approval level is required based on payment amount, whether supporting documentation is sufficient to authorize payment, and whether exception conditions warrant additional review or rejection.

Payments approved without proper verification, exposing the organization to fraud risk. New payee banking details not validated, creating vulnerability to business email compromise attacks. Approval thresholds not enforced, allowing payments to bypass required controls. Dual approval requirements circumvented, undermining separation of duties. Payment failures not caught promptly, causing missed payment deadlines and vendor relationship issues.

Orchestrates ACH payment approval across finance, treasury, and authorized signers in a controlled process that enforces organizational policy.

Validates payee details against master records and flags discrepancies or changes requiring additional verification.

Routes payments to appropriate approvers based on amount and type enforcing threshold and dual approval requirements.

AI agents check for duplicate payments and unusual patterns helping catch errors or potential fraud before authorization.

Captures complete approval records documenting who authorized each payment and under what conditions.

Connects to ERP, treasury, and banking systems to pull payment data and push approved transactions for transmission.