Finance director

FP&A manager

Chief financial officer

Department head

Controller

Budget analyst

This process is used when organizations establish spending authority for upcoming fiscal periods. It is triggered during annual budget planning cycles when departments submit their proposed allocations, when new initiatives require dedicated budget establishment, when organizational restructuring necessitates budget reallocation, or when board-level approval is required for overall financial plans. The process becomes essential when competing priorities must be balanced against available resources, when headcount and capital investments require authorization, or when budget commitments affect multi-year planning. Ideal for enterprises with multiple cost centers, organizations with formal governance requirements, nonprofits with restricted funding, and any business where disciplined resource allocation is critical to financial performance.

This process typically involves department heads or cost center managers who develop and submit budget proposals, budget analysts who review submissions for completeness and policy compliance, FP&A teams who consolidate departmental requests and analyze organizational impact, finance directors who evaluate alignment with financial targets and recommend adjustments, and executive leadership or the CFO who authorize final budget allocations. In some organizations, board finance committees review and approve overall budget frameworks before detailed allocations are finalized.

Aligned resource allocation ensuring spending plans support strategic priorities and business objectives. Clear spending authority with approved budgets establishing what departments are authorized to spend. Reduced budget cycle time by streamlining submission, review, and approval across multiple departments simultaneously. Documented approval chain tracking who proposed, reviewed, and authorized each budget component. Improved forecast accuracy when budget development includes rigorous justification and variance analysis.

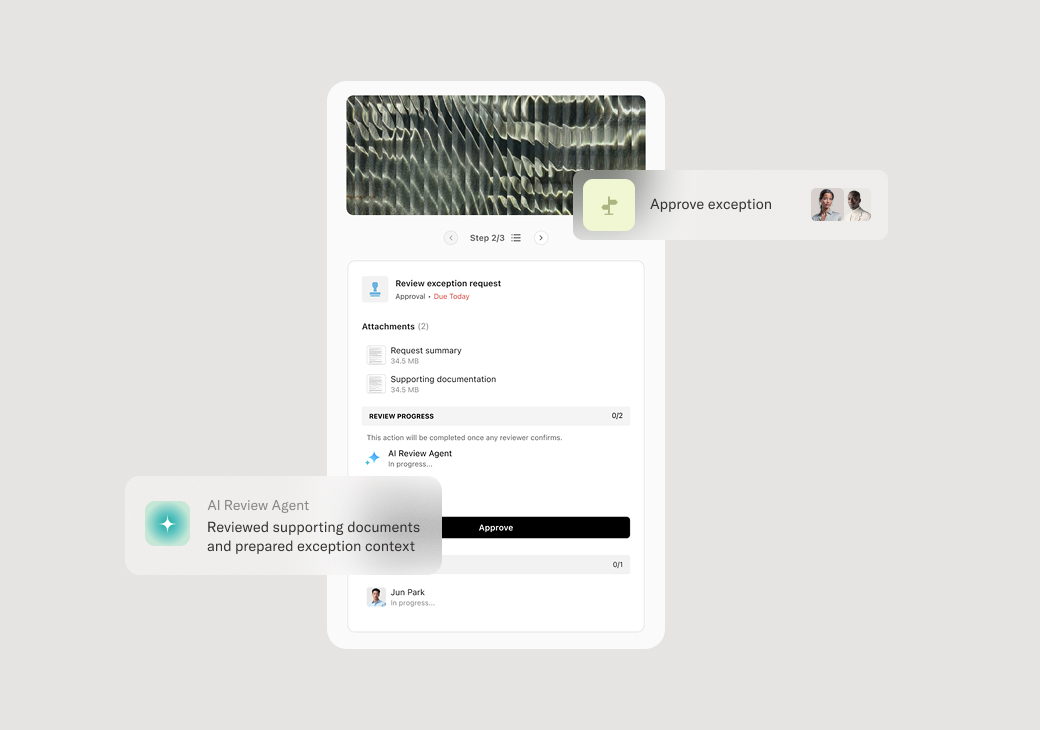

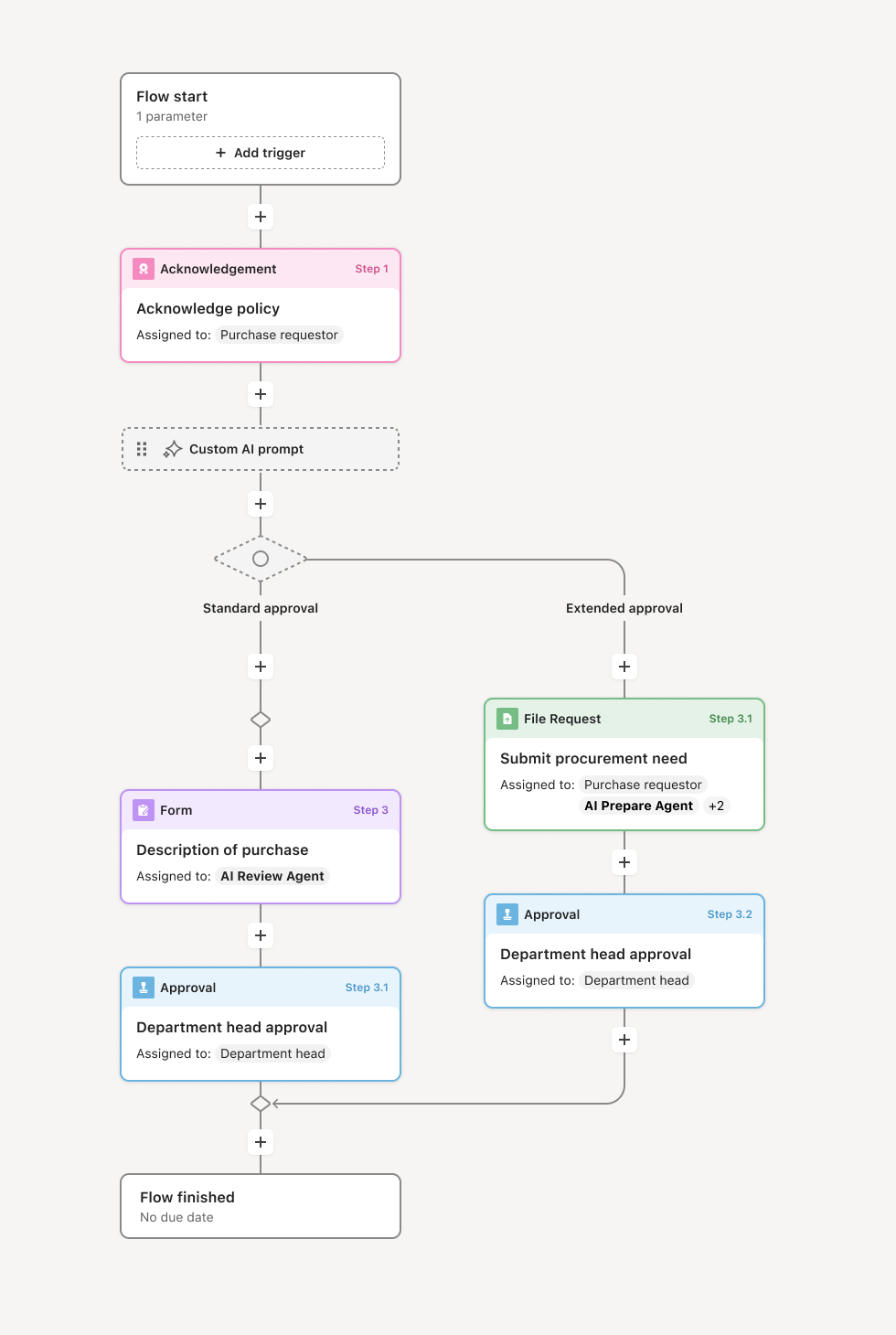

Your version of this process may vary based on roles, systems, data, and approval paths. Moxo's flow builder can be configured with AI agents, conditional branching, dynamic data references, and sophisticated logic to match how your organization runs this workflow. The steps below illustrate one example.

Budget submission and justification

The process begins when department heads submit their proposed budgets for the upcoming fiscal period. Submissions include line-item detail for personnel, operating expenses, capital investments, and any new initiative funding. Each request includes justification explaining how proposed spending supports departmental and organizational objectives, along with comparison to current period actuals and prior year budgets. An AI agent can assist by validating that submissions are complete, flagging significant variances from prior periods, and preparing summary comparisons for reviewers.

Finance review and variance analysis

Budget analysts and FP&A personnel review each submission for policy compliance, mathematical accuracy, and reasonableness. This includes analyzing year-over-year changes, comparing requests to historical spending patterns, and identifying items that require additional justification or appear inconsistent with organizational direction. If submissions contain errors or lack adequate support, they are returned to department heads for revision. Finance prepares variance analyses and consolidates departmental requests into an organizational view for leadership review.

Consolidation and prioritization

Finance consolidates all departmental submissions and compares total requests against available resources and revenue projections. If aggregate requests exceed funding capacity, prioritization discussions occur with department heads and leadership to align spending with strategic priorities. This phase may involve multiple iterations as trade-offs are negotiated and budgets are adjusted to fit within organizational constraints. The result is a balanced budget proposal that reflects both departmental needs and financial realities.

Executive review and adjustment

Senior leadership reviews the consolidated budget proposal, including the CFO, CEO, and relevant executive team members. This review assesses overall alignment with strategic objectives, adequacy of investment in growth priorities, appropriateness of cost management, and achievability of financial targets. Executives may request adjustments to specific line items or overall allocation percentages before providing approval. For significant budget decisions—such as major headcount changes or capital investments—additional discussion or board involvement may be required.

Final authorization and distribution

Once executive leadership approves the budget, final authorization is documented and approved allocations are communicated to department heads. Approved budgets are loaded into financial systems to establish spending authority and enable variance tracking throughout the fiscal period. The workflow records the complete approval chain, any conditions or restrictions attached to specific line items, and version history showing how the budget evolved through the approval process. Departments receive confirmation of their authorized spending levels and can proceed with planned activities.

This process commonly relies on inputs such as departmental budget templates, prior year actuals, current year forecasts, headcount plans, capital expenditure requests, strategic plan documentation, and revenue projections. It may be triggered by the annual planning calendar, a new fiscal year approaching, a significant organizational change, or board requirements for budget approval. Common systems that integrate with this workflow include ERP platforms like SAP, Oracle, or NetSuite, financial planning tools like Adaptive Insights or Anaplan, HRIS systems for headcount data, and spreadsheet tools where detailed budget models are maintained.

Key decision points include determining whether departmental submissions are complete and justified, whether aggregate requests fit within available resources, whether strategic priorities are adequately funded, and whether the overall budget meets financial targets and governance requirements. Each decision point may trigger requests for additional justification, negotiated adjustments between departments, escalation to executive leadership, or iteration on specific line items before final approval.

Incomplete submissions where missing justification or detail causes review cycles and delays the overall process. Unrealistic requests that significantly exceed available funding, requiring extensive negotiation and iteration. Disconnected from strategy when budget allocations do not reflect stated organizational priorities. Timeline compression where delayed submissions or reviews push final approval past the fiscal year start. Version confusion when multiple iterations create uncertainty about which budget numbers are current and approved.

Orchestrates the complete budget cycle from departmental submission through finance review, consolidation, executive approval, and distribution in a single coordinated flow.

Manages parallel departmental submissions so multiple cost centers can submit and iterate simultaneously without bottlenecking the process.

AI agents analyze variances and completeness flagging significant changes from prior periods and identifying missing justification before human review.

Connects to ERP and planning systems so historical data flows in automatically and approved budgets can be loaded into financial systems.

Maintains version history and approval records tracking how budgets evolved through iterations and who authorized final allocations.

Enforces planning calendar deadlines with automated reminders ensuring submissions and reviews stay on schedule for fiscal year readiness.