Credit manager

Accounts receivable manager

Finance controller

Risk analyst

Sales operations manager

Treasury manager

When establishing initial credit limits for new customers. When customers request limit increases based on growing order volumes. When periodic reviews indicate limits should be adjusted. Ideal for wholesalers, distributors, manufacturers, and any B2B organization extending trade credit.

Sales teams initiate limit requests based on customer needs. Credit analysts evaluate financial data and payment history. Credit managers approve limits within their authority. Senior leaders or committees authorize limits exceeding standard thresholds. AR teams implement approved limits in billing systems.

Appropriate credit exposure aligned with customer risk profiles and business needs Faster limit decisions enabling sales teams to close deals without credit delays Reduced overexposure risk through consistent limit-setting criteria Clear limit history documenting all adjustments and their rationale

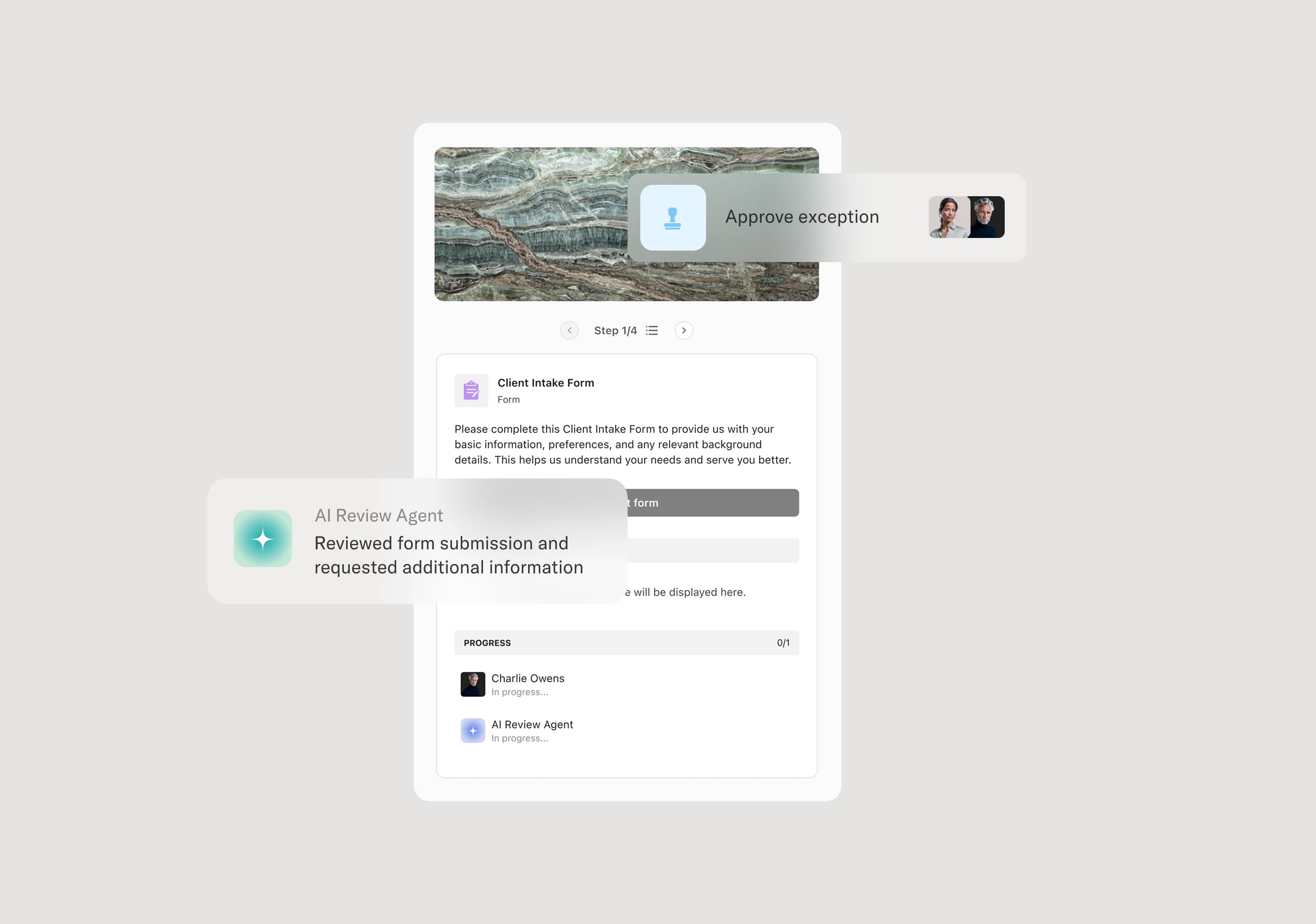

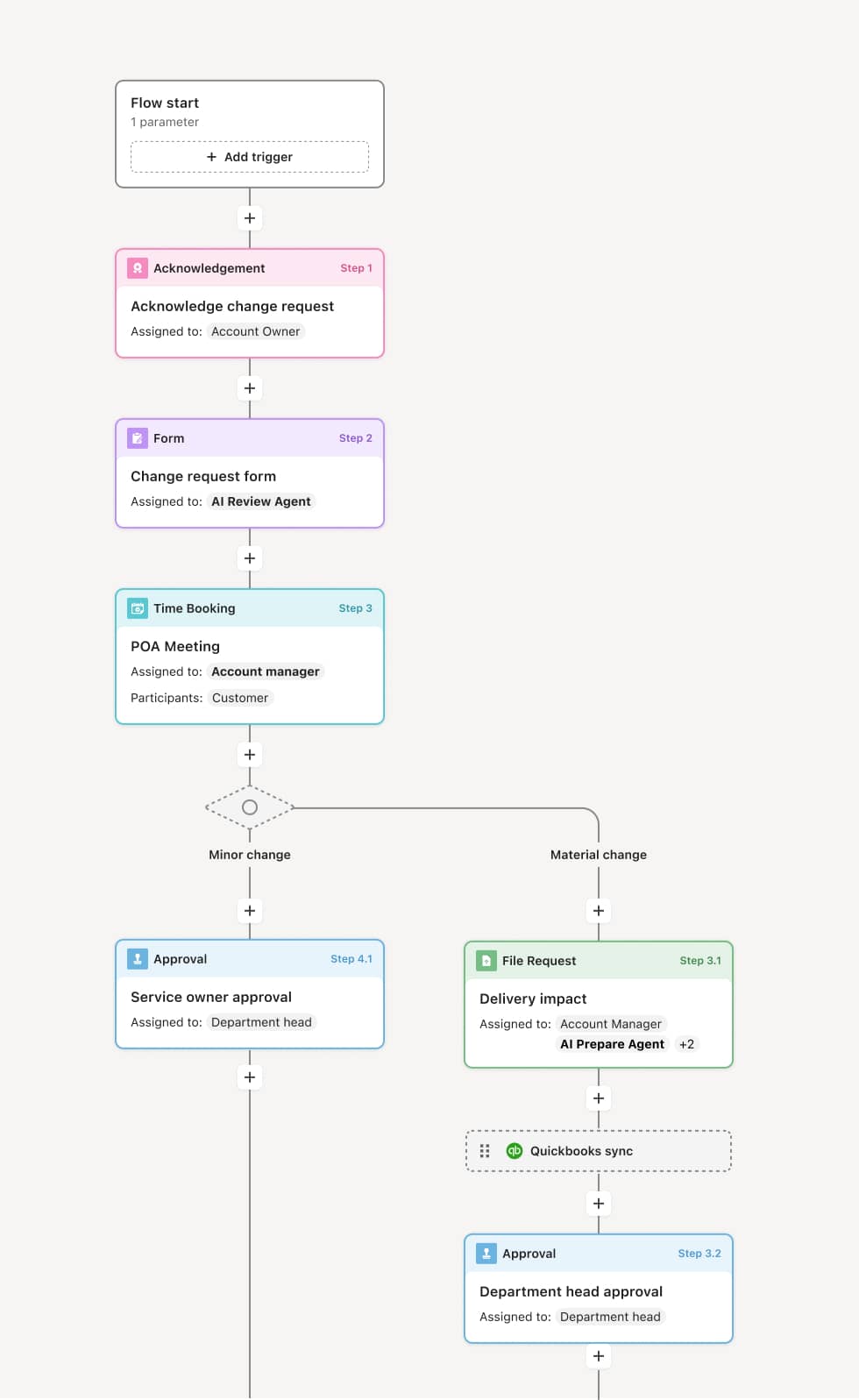

Your version of this process may vary based on roles, systems, data, and approval paths. Moxo's flow builder can be configured with AI agents, conditional branching, dynamic data references, and sophisticated logic to match how your organization runs this workflow. The steps below illustrate one example.

Limit request initiation

The process begins when a limit request is submitted, either for a new customer or an increase on an existing account. An AI agent may pull current credit data, payment history, and existing exposure to provide context for evaluation.

Credit evaluation

Credit analysts review financial information, credit bureau data, and internal payment history. The analyst calculates a recommended limit based on policy guidelines and documents their assessment. AI agents may flag discrepancies or highlight risk factors.

Limit approval decision

Based on the evaluation, an approver with appropriate authority reviews the recommendation. If the requested limit exceeds standard thresholds, the workflow routes to senior approvers. The approver may approve the recommended limit, set a different limit, or decline.

Implementation and communication

Approved limits are updated in credit management and ERP systems. The customer and sales team are notified of the approved limit. If the limit differs from the request, the rationale is communicated.

Periodic review scheduling

The workflow may schedule periodic limit reviews based on account type or risk level. When review dates arrive, the process reinitiates to reassess limits based on current data.

This process relies on customer financial data, credit bureau reports, internal payment history, current exposure data, and policy guidelines. Triggers include new customer applications, sales requests, or scheduled periodic reviews. Integration with credit bureaus, ERP systems like SAP or Oracle, and CRM platforms provides comprehensive data access.

Key decision points include determining whether the customer meets minimum credit criteria, what limit is appropriate given their risk profile, and whether the requested limit exceeds approval authority thresholds.

Outdated financial data leading to inappropriate limits. Limits approved without considering current exposure across related entities. Approved limits not updated in billing systems causing order holds. Lack of periodic review allowing limits to become misaligned with current risk.

Orchestrates limit evaluation and approval across analysts and approvers with clear handoffs

AI agents validate data completeness and surface relevant context for evaluation

Routes requests to appropriate authority levels based on limit amount and customer risk tier

Schedules periodic reviews ensuring limits remain appropriate over time