KYC compliance manager

Onboarding operations lead

BSA/AML compliance officer

Relationship manager

Compliance analyst

Customer operations director

This process is used when an individual customer applies to open an account or establish a relationship that requires identity verification under CIP, CDD, and AML regulations. It applies when the customer’s identity must be verified through documentary or non-documentary methods, the customer must be screened against sanctions, PEP, and adverse media databases, and a risk assessment must be completed before the relationship is approved. Ideal for banks, credit unions, broker-dealers, fintech companies, insurance companies, and any financial institution subject to CIP and CDD requirements.

The KYC verification process typically involves onboarding specialists who collect and review customer identification, KYC analysts who verify identity and conduct screening, compliance officers who review high-risk customers and approve the relationship, the customer who provides identification and personal information, and relationship managers who manage the customer interaction.

Verified customer identity confirmed through government-issued identification and independent verification sources. Screened customer risk with every customer checked against sanctions, PEP, and adverse media databases before onboarding. Risk-rated relationship with each customer assigned a risk rating that drives the level of ongoing monitoring and review. CIP and CDD compliance demonstrated through documented verification, screening, and risk assessment records. Streamlined onboarding that collects identification, verifies identity, and completes screening without unnecessary friction for the customer.

Your version of this process may vary based on roles, systems, data, and approval paths. Moxo’s flow builder can be configured with AI agents, conditional branching, dynamic data references, and sophisticated logic to match how your organization runs this workflow. The steps below illustrate one example.

Customer information collection

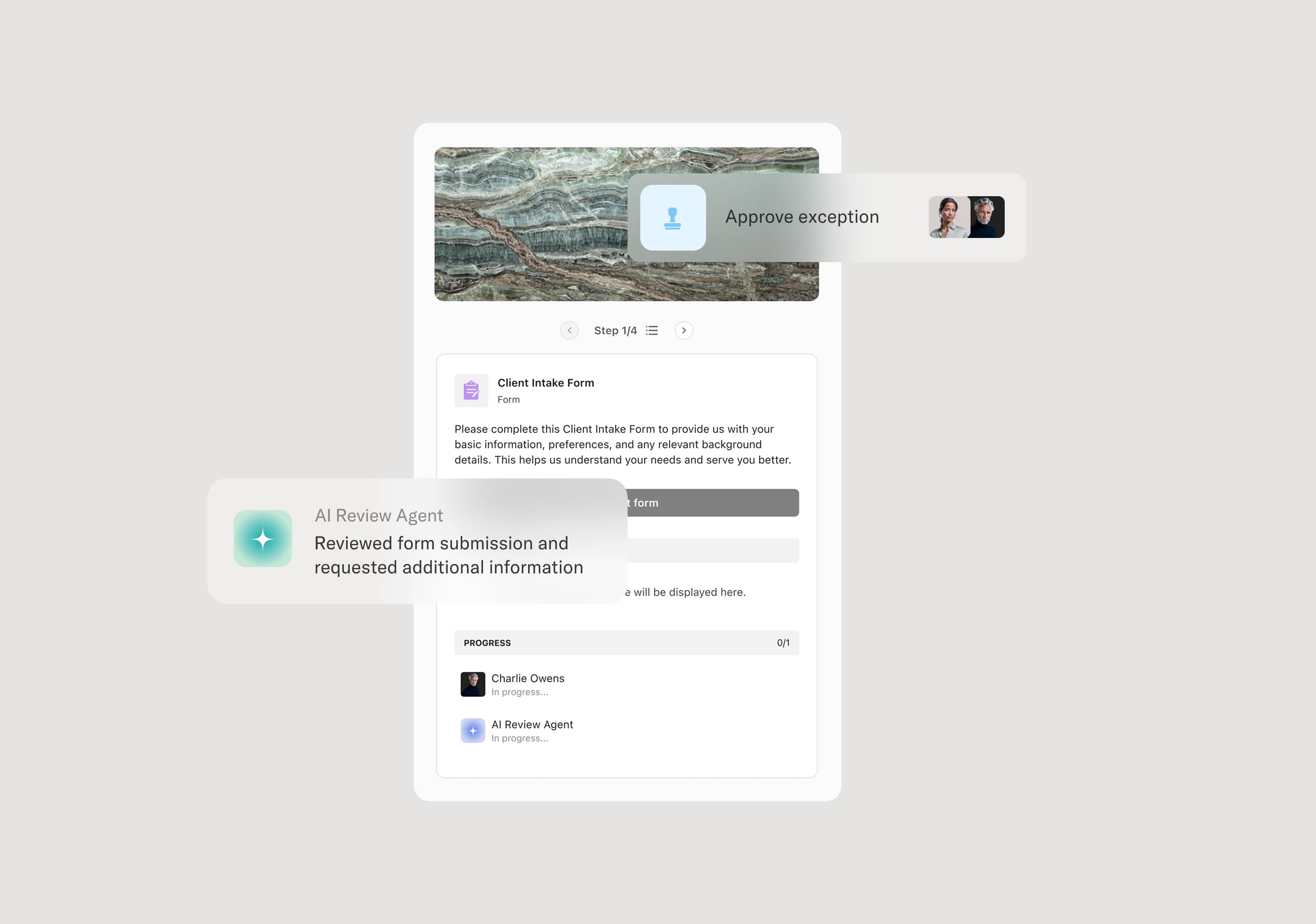

The process begins when the customer provides their personal information and identification as part of the onboarding application. Required information typically includes full legal name, date of birth, address, identification number (such as SSN or taxpayer ID), and a government-issued photo identification document. An AI Agent can assist by verifying the application for completeness and prompting the customer for any missing information.

Identity verification

The KYC analyst verifies the customer’s identity through documentary verification (reviewing the government-issued ID for authenticity) and non-documentary verification (cross-referencing identity data against independent databases). Identity verification confirms that the person is who they claim to be and that the identification documents are valid.

Screening

The customer is screened against sanctions lists (OFAC SDN, EU, UN), PEP databases, and adverse media sources. Any potential matches are reviewed by the analyst to determine whether they are true matches or false positives. True matches are escalated to compliance for further review and disposition. An AI Agent may run the screening automatically and categorize results for analyst review.

Risk assessment and rating

The analyst assesses the customer’s risk based on factors including geographic risk, occupation or source of income, product type, and screening results. The customer is assigned a risk rating — low, medium, or high — that determines the level of ongoing transaction monitoring and the frequency of periodic review.

Relationship approval

Standard-risk customers are approved at the analyst level. High-risk customers require senior compliance review and approval before onboarding proceeds. If the customer cannot be verified or screening reveals prohibitive risk, the relationship is declined with documented rationale.

Ongoing monitoring and periodic review

Approved customers are entered into the ongoing monitoring program. Transaction monitoring is calibrated to the customer’s risk rating. Periodic KYC reviews refresh the customer’s profile at intervals determined by risk level.

This process commonly relies on inputs such as the customer’s personal information, government-issued identification documents, identity verification results, and screening results. It may be triggered by a new account application. Connected systems often include KYC platforms like Jumio, Onfido, or Fenergo, identity verification services, sanctions screening tools like Refinitiv or Dow Jones, and the organization’s core banking or onboarding platform.

Key decision points include whether the customer’s identity is verified through acceptable documentary and non-documentary methods, whether screening results reveal sanctions matches, PEP status, or adverse media requiring enhanced review, what risk rating is appropriate based on the customer’s profile, and whether high-risk customers should be approved, approved with conditions, or declined.

Identity verification incomplete because the identification document was not authenticated or non-documentary verification was not performed. Screening matches not reviewed, allowing potential sanctions or PEP exposure to pass without assessment. Risk rating not assigned or defaulted to a standard level without consideration of actual risk factors. High-risk customers approved without senior review, creating compliance gaps. KYC records not maintained with sufficient documentation for regulatory examination.

Orchestrates KYC verification from application through approval and ongoing monitoring across onboarding, compliance, and the customer in a single coordinated flow.

Engages customers within the workflow for identification submission, information collection, and status communication, creating a streamlined onboarding experience.

AI Agents verify application completeness, run automated sanctions, PEP, and adverse media screening, and categorize matches for analyst review.

Routes high-risk customers for senior compliance review within the workflow with full verification and screening context.

Connects to KYC platforms, identity verification services, and screening tools like Jumio, Onfido, Refinitiv, and Dow Jones so verification data flows into the customer’s compliance record.

Preserves the complete KYC record including identification, verification results, screening, risk assessment, and approval documentation for CIP, CDD, and examination readiness.