Loan operations manager

Underwriting director

BSA/AML compliance officer

Mortgage processing supervisor

Credit risk manager

Lending compliance lead

This process is used when an individual or business applies for a loan, mortgage, line of credit, or other lending product that requires identity verification, financial assessment, and regulatory screening as part of the origination process. It applies when the applicant’s identity must be verified under CIP, their financial standing must be assessed for creditworthiness, and their risk profile must be screened for AML, sanctions, and fraud concerns. Ideal for banks, credit unions, mortgage lenders, fintech lending platforms, and any organization originating consumer or commercial credit.

The loan application KYC process typically involves loan processors who collect and review application documentation, KYC analysts who verify identity and conduct regulatory screening, underwriters who assess creditworthiness and financial standing, compliance officers who review high-risk applications, and the applicant who provides identification, financial documentation, and disclosures.

Verified applicant identity confirmed before the credit decision, meeting CIP and CDD requirements within the lending context. Validated income and financial standing through documentation that supports the underwriting assessment. Screened applicant risk with every applicant checked against sanctions, PEP, adverse media, and fraud databases. Compliant loan origination that integrates KYC into the lending workflow rather than treating it as a separate compliance exercise. Reduced fraud and default risk by identifying identity fraud, misrepresented income, and regulatory risk indicators before funding.

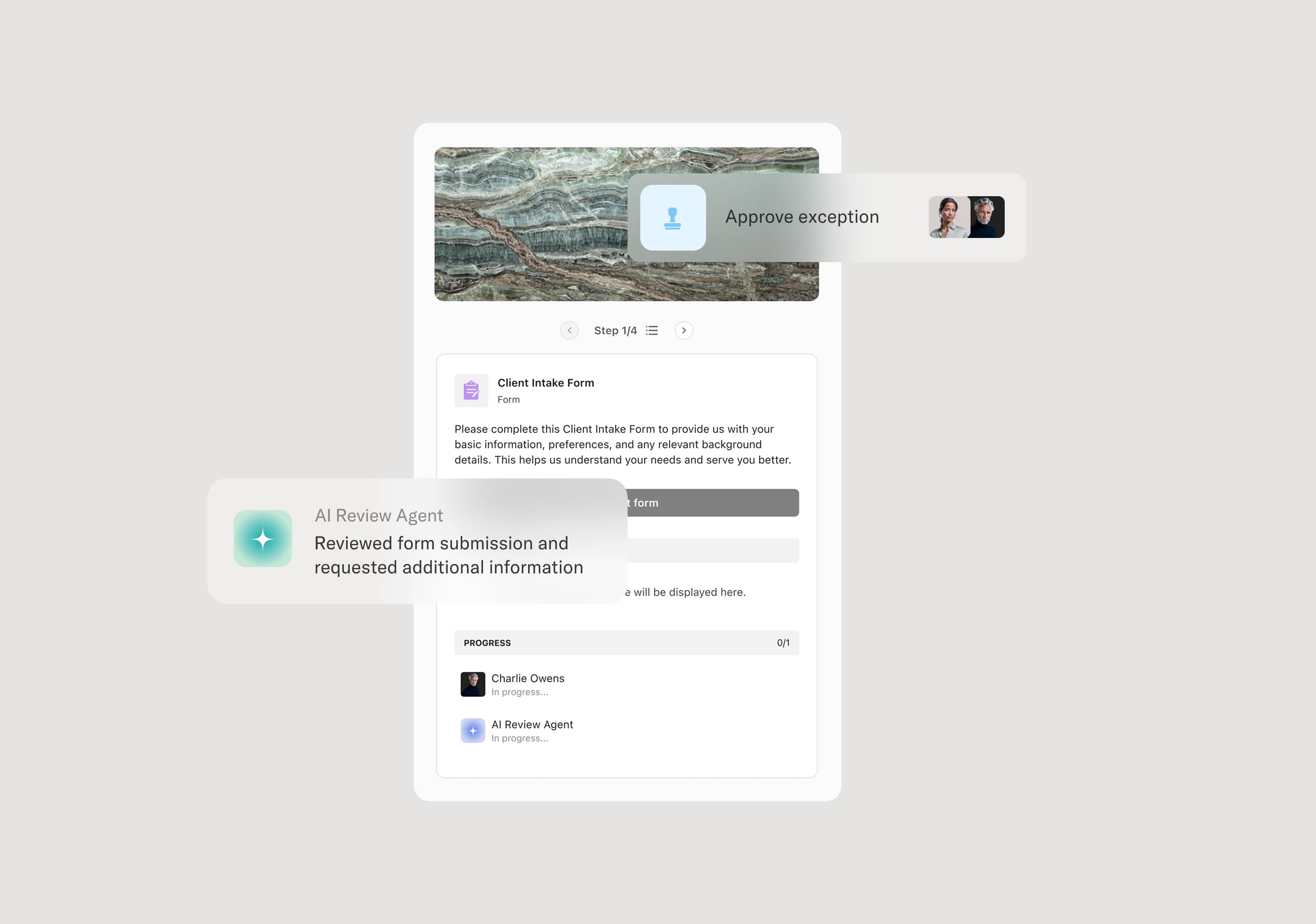

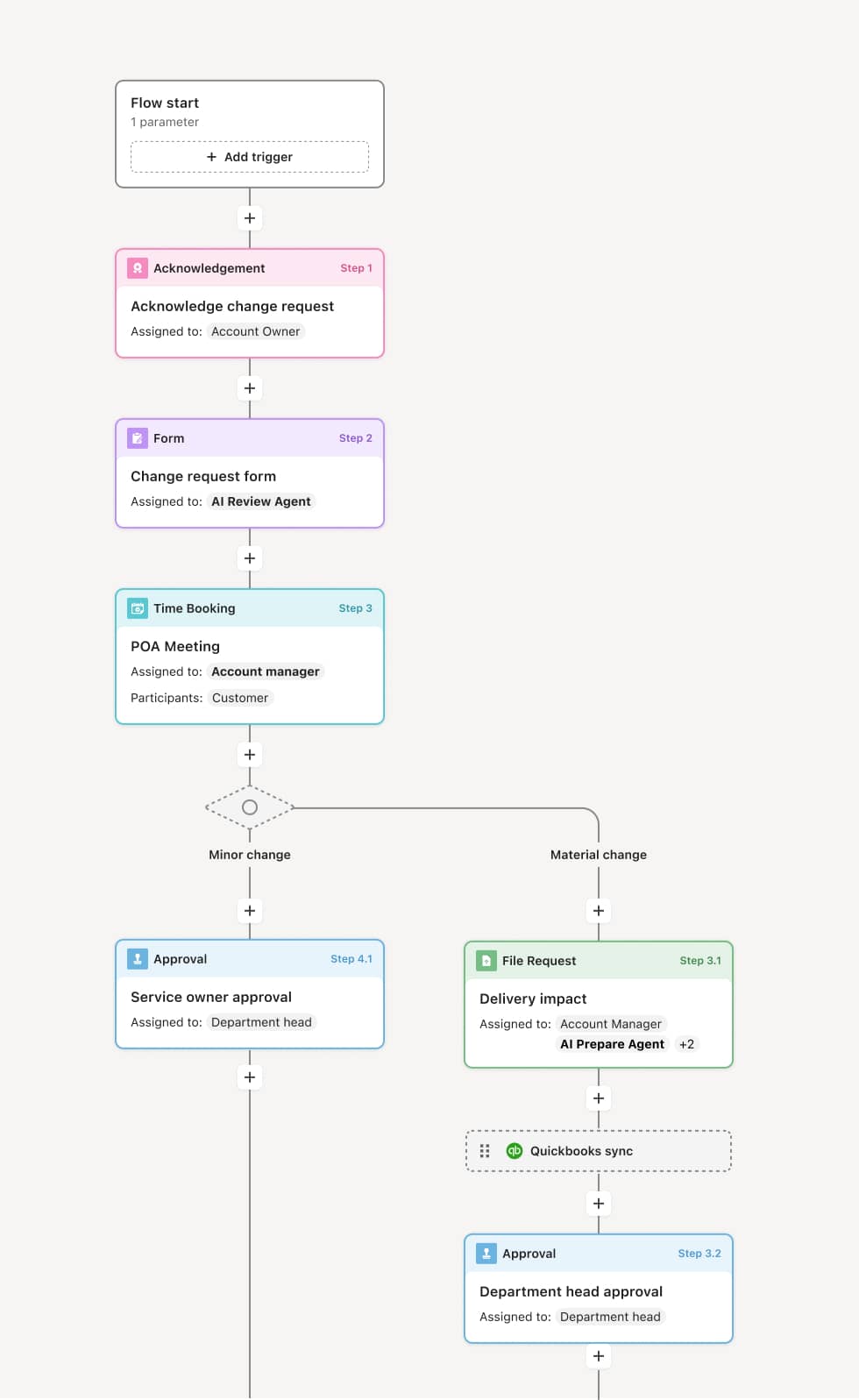

Your version of this process may vary based on roles, systems, data, and approval paths. Moxo’s flow builder can be configured with AI agents, conditional branching, dynamic data references, and sophisticated logic to match how your organization runs this workflow. The steps below illustrate one example.

Application intake and document collection

The process begins when the applicant submits a loan application with required documentation, including government-issued identification, proof of income (pay stubs, tax returns, bank statements), employment verification, and asset documentation as applicable to the loan type. An AI Agent can assist by verifying document completeness against the loan product’s documentation requirements and prompting the applicant for missing items.

Identity verification

The KYC analyst verifies the applicant’s identity using government-issued identification and independent verification sources, consistent with CIP requirements. For joint applications, all applicants are verified individually. Identity verification is completed before the underwriting assessment proceeds.

Regulatory screening

The applicant is screened against OFAC sanctions lists, PEP databases, adverse media, and fraud databases. Any screening alerts are reviewed and resolved. High-risk screening results are escalated to compliance before the application proceeds. An AI Agent may run screening automatically and flag alerts for analyst review.

Income and financial verification

The loan processor verifies the applicant’s income, employment, and financial standing using submitted documentation and, where applicable, third-party verification services. The verification confirms that the applicant’s financial profile supports the requested loan amount and terms.

Underwriting assessment

The underwriter reviews the verified identity, financial documentation, credit report, and screening results as part of the credit decision. The underwriting assessment considers the applicant’s ability to repay, collateral value (for secured loans), and overall risk profile. An AI Agent may compile the complete application package with all verification and screening results for the underwriter’s review.

Decision and documentation

The credit decision — approved, approved with conditions, or declined — is made based on the combined KYC, financial, and credit assessment. All verification, screening, and underwriting documentation is preserved in the loan file. If approved, the application proceeds to closing and funding.

This process commonly relies on inputs such as the loan application, government-issued identification, proof of income, tax returns, bank statements, employment verification, credit reports, and screening results. It may be triggered by a loan application submission. Connected systems often include loan origination systems (LOS) like Encompass, Blend, or nCino, KYC and identity verification platforms, credit bureaus, income verification services, and sanctions screening tools.

Key decision points include whether the applicant’s identity is verified to CIP standards, whether screening results reveal sanctions, PEP, fraud, or adverse media indicators requiring escalation, whether income and financial documentation support the requested loan amount, and whether the combined KYC and financial assessment supports the credit decision.

Identity verification not completed before underwriting, allowing credit decisions to be made for unverified applicants. Income documentation not verified against independent sources, creating exposure to income misrepresentation. Screening results not reviewed before the credit decision, allowing sanctioned or high-risk applicants to proceed. KYC and underwriting treated as separate processes with poor information flow between them, causing duplication and delays. Loan file documentation incomplete at closing, creating compliance gaps during post-close audit or regulatory examination.

Orchestrates loan application KYC from application intake through credit decision across loan processors, KYC analysts, underwriters, compliance, and the applicant in a single coordinated flow.

Engages applicants within the workflow for document submission, identity verification, and status updates, reducing back-and-forth and application abandonment.

AI Agents verify document completeness against loan product requirements, run automated regulatory screening, and compile the full application package for underwriting review.

Integrates KYC verification with the underwriting workflow so identity, screening, and financial verification results flow into the credit decision rather than operating in a separate compliance silo.

Connects to loan origination systems, KYC platforms, and credit bureaus like Encompass, nCino, Jumio, and TransUnion so application data, verification results, and credit data are synchronized.

Preserves the complete loan KYC record including identity verification, screening, income validation, and credit assessment documentation for post-close audit and regulatory examination.