Collections manager

Account manager

Finance controller

Credit analyst

Revenue operations lead

Billing operations manager

This process is used when a customer or client requests an alternative to a lump-sum payment, typically due to financial difficulty, disputed charges, or a need to spread costs over time. It is triggered when an account becomes past due, when a customer formally requests installment terms, or when a collections team identifies that a structured plan is more likely to recover the outstanding balance than continued collection efforts. Payment plan approval is common across financial services, healthcare, telecommunications, professional services, and any organization that extends credit or manages receivables.

Payment plan approval typically involves the requesting party, whether a customer, client, or debtor, an account manager or collections specialist who gathers context and proposes terms, a credit analyst who evaluates payment history and risk, and a finance controller or revenue operations lead who provides final approval on the plan structure. Legal or compliance teams may also be involved when plans carry regulatory requirements or when the balance exceeds a defined threshold.

Higher recovery rates by offering structured repayment options that reduce the likelihood of write-offs or default. Consistent plan terms through policy-driven evaluation that ensures similar accounts receive similar treatment. Faster resolution of past-due balances by moving accounts from collections limbo into approved, trackable repayment commitments. Clear accountability for plan authorization with every approval, modification, and exception tied to a specific decision-maker and documented in the process record.

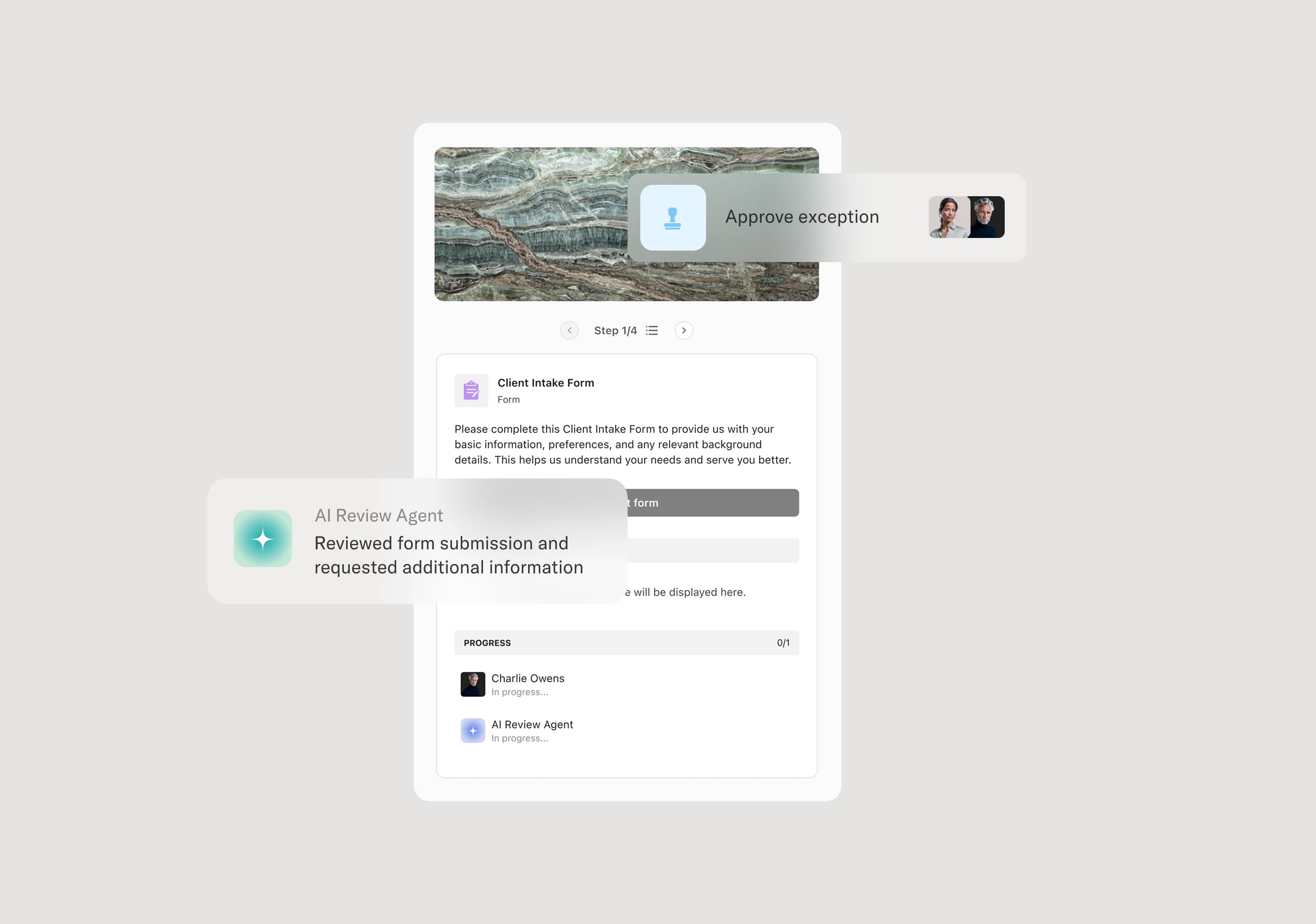

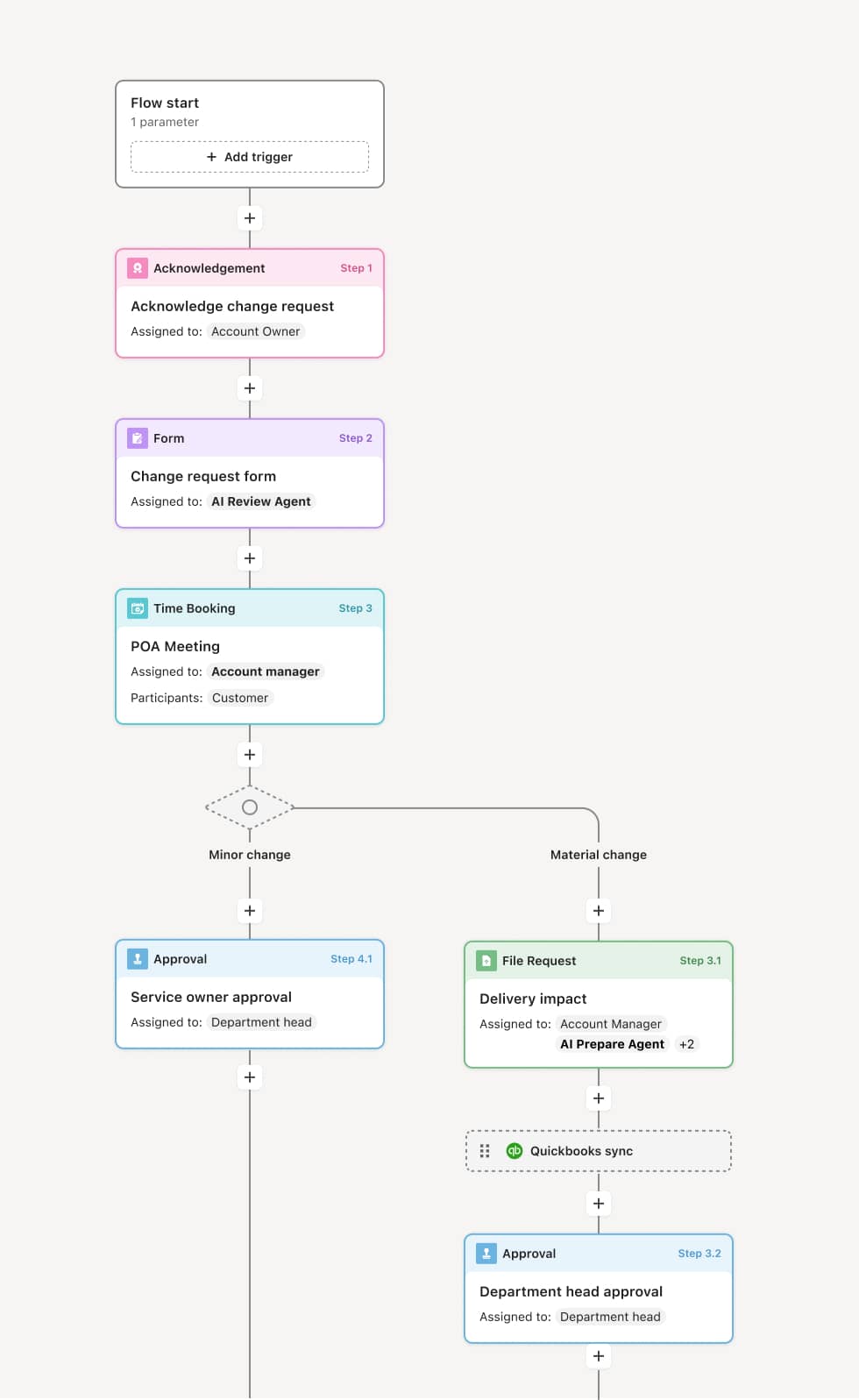

Your version of this process may vary based on roles, systems, data, and approval paths. Moxo’s flow builder can be configured with AI agents, conditional branching, dynamic data references, and sophisticated logic to match how your organization runs this workflow. The steps below illustrate one example.

Request and context gathering

The process begins when a payment plan is requested, either by the customer directly or by an account manager who determines that a structured plan is the most effective path to recovery. The request includes details such as the outstanding balance, account history, reason for the request, and any proposed terms. An AI Agent may prepare a summary of the account's payment history, prior plans, and current standing to give reviewers immediate context without requiring manual research.

Risk and eligibility assessment

The request is routed to a credit analyst or collections specialist who evaluates the account against the organization's payment plan policy. This includes reviewing factors such as total balance, payment behavior, existing plan history, and any associated disputes. If the account meets standard eligibility criteria, the plan may proceed to approval with recommended terms. If the account falls outside standard parameters, the process branches to a more detailed risk assessment or requires additional documentation from the requesting party.

Plan structuring

With eligibility confirmed, the proposed plan terms are finalized. This includes the installment schedule, payment amounts, duration, any interest or fees, and consequences for non-compliance. The account manager or collections specialist may negotiate terms with the customer within policy-defined boundaries. If the terms require deviation from standard policy, such as extended duration or reduced total recovery, the plan is flagged for escalated review.

Approval or escalation

The structured plan is routed to the appropriate approver based on the balance amount, plan duration, or deviation from policy. Standard plans may be approved by a collections manager, while high-value or non-standard plans require sign-off from a finance controller or revenue operations lead. The approver reviews the complete package, including account context, risk assessment, proposed terms, and any negotiation history, before authorizing or requesting modifications.

Agreement execution and monitoring

Once approved, the payment plan agreement is formalized and shared with the customer for acceptance. This may include an e-signature step or an acknowledgment of the plan terms. Upon acceptance, the plan is activated and the account is transitioned from collections to scheduled repayment. All terms, approvals, and acceptance records are retained as part of the process, and the plan can be monitored for compliance throughout its duration.

This process commonly relies on inputs such as account balance data, payment history, customer or client contact information, prior plan records, and policy guidelines for plan eligibility. It may be triggered by a customer request, a collections team recommendation, or an automated flag from a billing or CRM system. Systems such as Salesforce, NetSuite, or a collections platform may provide account data, balance details, and transaction history.

Key decision points include whether the account meets eligibility criteria for a payment plan, whether the proposed terms fall within standard policy or require exception approval, whether the balance or plan duration exceeds thresholds that trigger escalation, and whether the customer accepts or requests modifications to the proposed terms.

Inconsistent eligibility assessments, when different analysts apply different criteria to similar accounts, leading to uneven treatment and potential disputes. Stalled negotiations, when the customer and collections team cannot reach agreement on terms and no clear escalation path exists. Missing approval authority, when non-standard plans sit in queue because the required approver is unclear or unavailable. Plan activation delays, when the gap between approval and customer acceptance allows the account to continue aging without resolution.

Orchestrates the full payment plan lifecycle from initial request through risk assessment, plan structuring, approval, and customer acceptance in a single coordinated process.

AI Agents prepare account summaries and flag policy exceptions so reviewers enter each decision point with full context rather than spending time pulling data from multiple systems.

Routes plans to the right approver based on balance, duration, and policy deviation ensuring standard plans move quickly while exceptions receive the appropriate level of review.

Extends existing billing and CRM systems such as Salesforce or NetSuite by connecting account data and payment history directly into the approval workflow.

Captures a complete record of every assessment, negotiation, approval, and customer acceptance so finance teams can trace any active plan back to its originating request and authorization chain.