Fraud operations manager

Customer service director

Fraud investigations lead

Compliance officer

Risk management director

Payments operations manager

This process is used when a customer reports suspected fraud on their account or when the organization’s fraud detection systems identify potentially fraudulent activity that requires customer notification and case management. It applies when the case must be tracked through investigation, the customer must receive provisional credit and status updates within regulatory timeframes (such as Regulation E for electronic fund transfers), and the account must be secured and remediated. Ideal for banks, credit unions, payment processors, fintech companies, and any financial institution managing customer fraud cases.

The fraud case management process typically involves fraud operations analysts who manage the case lifecycle, customer service representatives who handle the initial report and ongoing customer communication, fraud investigators who analyze the transactions and determine fraud, compliance staff who ensure regulatory timeframe compliance, and the affected customer who provides information, receives updates, and completes remediation steps.

Regulatory-compliant case handling with provisional credits, investigation timelines, and customer notifications meeting Regulation E and organizational requirements. Protected customer accounts through prompt security measures that prevent further unauthorized activity. Timely case resolution because each case is tracked against investigation deadlines and escalated when at risk of exceeding timeframes. Informed customers who receive consistent updates on their case status and resolution. Complete case documentation supporting regulatory examination, chargeback processing, and loss recovery.

Your version of this process may vary based on roles, systems, data, and approval paths. Moxo’s flow builder can be configured with AI agents, conditional branching, dynamic data references, and sophisticated logic to match how your organization runs this workflow. The steps below illustrate one example.

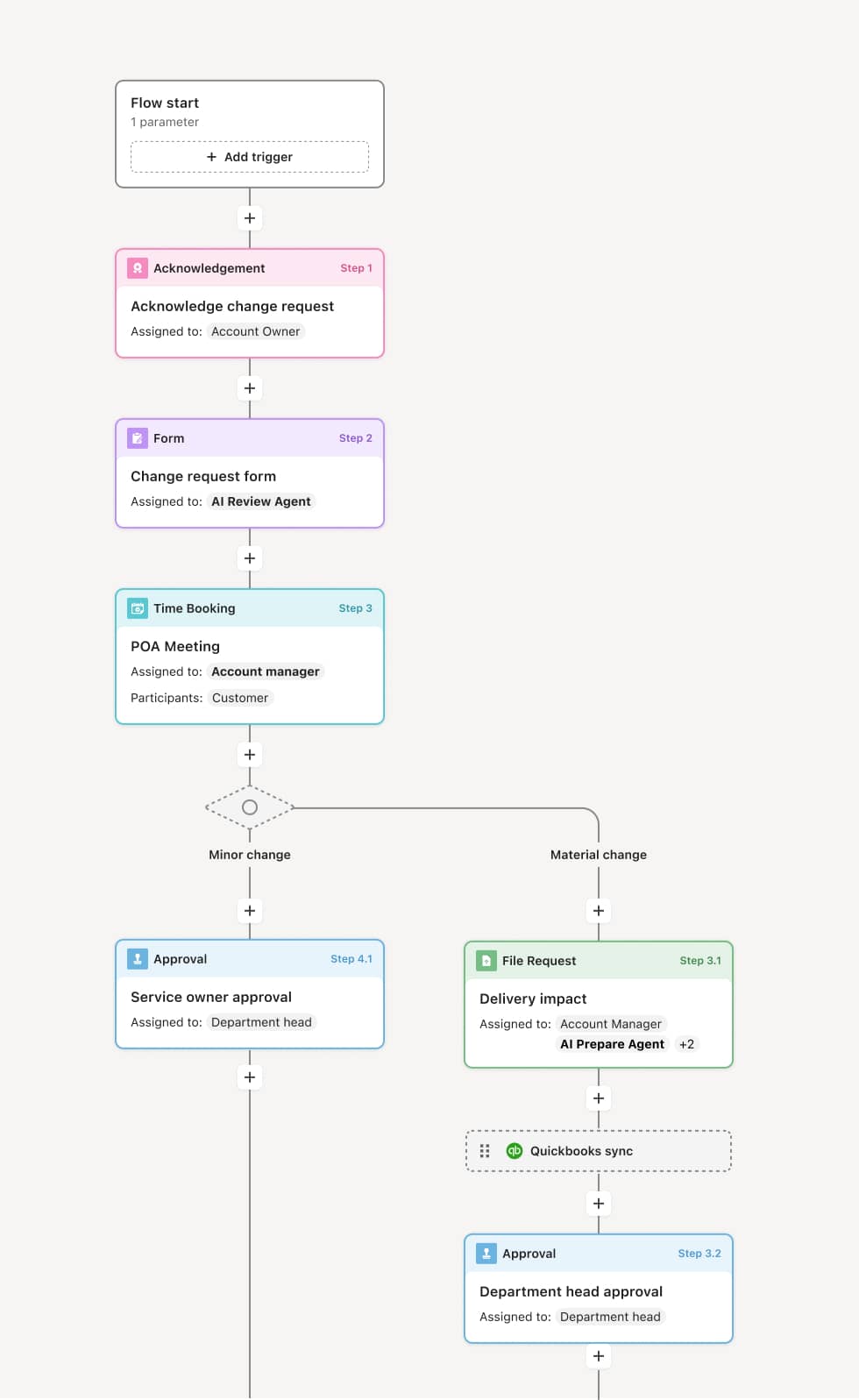

Fraud report intake and account protection

The process begins when a customer reports suspected fraud or when the organization’s detection systems flag potentially fraudulent transactions. The fraud operations analyst captures the report details, affected transactions, and the customer’s account information. Immediate account protection measures are taken, which may include blocking the compromised card, locking online access, or placing a fraud alert on the account. An AI Agent can assist by pulling the transaction history, account activity, and any prior fraud reports for the customer.

Provisional credit and regulatory notification

If the case involves electronic fund transfers, the organization provides provisional credit to the customer within the timeframe required by Regulation E (typically 10 business days). The customer is notified of their rights, the investigation timeline, and the provisional credit. The regulatory clock is tracked from the date of the customer’s report.

Transaction investigation

The fraud analyst or investigator reviews the disputed transactions, analyzing transaction patterns, device and location data, merchant information, and any available surveillance or authentication records. The investigation determines whether each transaction is confirmed fraud, authorized by the customer, or inconclusive. An AI Agent may cross-reference the flagged transactions against known fraud patterns and prior case history.

Resolution determination

Based on the investigation, the case is resolved: confirmed fraud transactions result in permanent credit to the customer, unauthorized access is documented for loss recovery, and any transactions found to be authorized are reversed from the provisional credit with customer notification. The customer is informed of the determination and their dispute rights if they disagree.

Account remediation and restoration

After the fraud is resolved, the customer’s account is remediated. This may include issuing new account credentials, resetting security settings, removing fraudulent transactions from the account history, and confirming that the account is fully restored.

Case closure and loss recovery

The case is closed with a complete record of the report, investigation, determination, and remediation. If applicable, loss recovery actions such as chargebacks, insurance claims, or law enforcement referrals are initiated.

This process commonly relies on inputs such as the customer’s fraud report, transaction records, account activity, device and authentication data, and merchant information. It may be triggered by a customer report, a fraud detection alert, or a chargeback notification. Connected systems often include fraud case management platforms, core banking systems, card management platforms, authentication systems, and chargeback processing tools.

Key decision points include whether the customer’s account requires immediate protection measures, whether provisional credit is required under Regulation E and within what timeframe, whether each disputed transaction is confirmed fraud, authorized, or inconclusive, and whether the case warrants loss recovery actions such as chargebacks or law enforcement referral.

Provisional credit not issued within the regulatory timeframe, creating compliance violations. Account protection measures delayed, allowing additional unauthorized transactions after the fraud is reported. Investigation not completed within the required timeframe (typically 45 to 90 days under Regulation E), resulting in provisional credits becoming permanent regardless of the investigation outcome. Customer not informed of investigation status or resolution, damaging trust and generating complaints. Loss recovery not pursued for confirmed fraud cases, leaving recoverable losses on the organization’s books.

Orchestrates fraud case management from customer report through resolution and account remediation across fraud operations, customer service, investigations, and the customer in a single coordinated flow.

Triggers immediate account protection actions within the workflow when fraud is reported, preventing further unauthorized activity.

Tracks regulatory timeframes for provisional credit, investigation completion, and customer notification, alerting the team when deadlines are approaching.

Engages customers within the workflow for fraud report details, status updates, and remediation confirmation, keeping all communications documented.

Connects to core banking, card management, and fraud platforms so transaction data, account actions, and case documentation are synchronized.

Preserves the complete case record including the fraud report, investigation analysis, determination, customer communications, remediation actions, and loss recovery for regulatory examination and audit.