Fraud operations manager

Customer service supervisor

Dispute intake coordinator

Compliance officer

Payments operations lead

Call center manager

This process is used whenever a customer contacts the organization to report suspected fraud on their account, or when fraud detection systems generate alerts requiring customer confirmation. It applies when the initial report must capture sufficient detail about the disputed transactions, the customer’s account, and the circumstances to enable accurate classification, immediate account protection, and investigation routing. It is common when customer service, fraud operations, and the customer must coordinate quickly under regulatory time pressure. Ideal for banks, credit unions, payment processors, and fintech companies handling customer fraud reports at scale.

The fraud dispute intake process typically involves customer service representatives who receive the initial report and capture claim details, fraud intake specialists who validate and classify the claim, fraud operations analysts who receive routed cases for investigation, compliance staff who monitor regulatory timeframe adherence, and the customer who provides the fraud report and supporting information.

Complete initial documentation that captures all details needed to support investigation without requiring re-contact with the customer. Accurate claim classification that routes the case to the correct investigation team based on fraud type, channel, and severity. Immediate account protection triggered at the point of intake to prevent further unauthorized activity. Regulatory timeframe compliance because the intake date is captured precisely and the investigation clock begins without delay. Reduced customer effort through a guided intake experience that collects all required information in a single interaction.

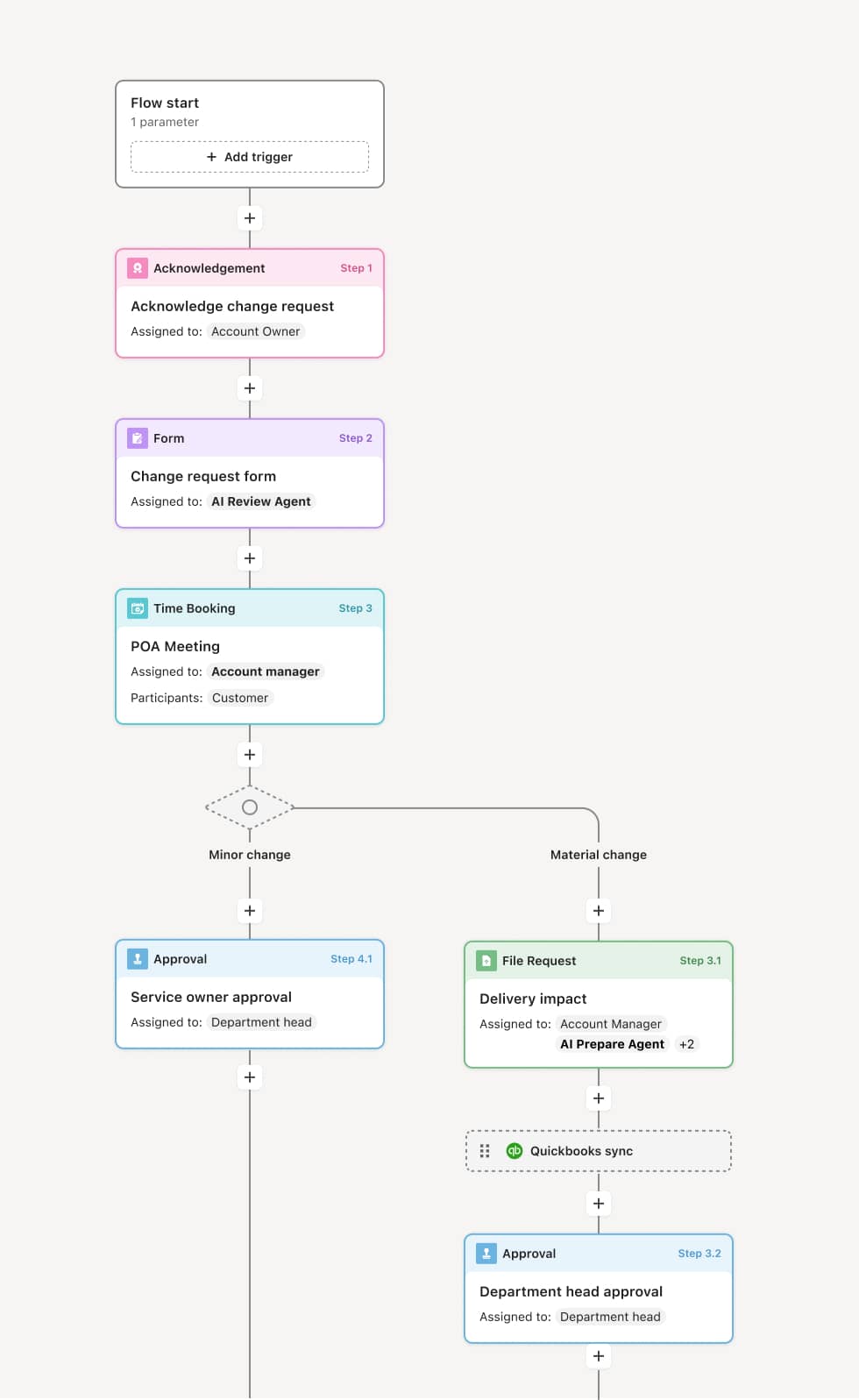

Your version of this process may vary based on roles, systems, data, and approval paths. Moxo’s flow builder can be configured with AI agents, conditional branching, dynamic data references, and sophisticated logic to match how your organization runs this workflow. The steps below illustrate one example.

Customer contact and identity verification

The process begins when a customer contacts the organization to report suspected fraud. The representative verifies the customer’s identity through the organization’s authentication protocol before proceeding with the fraud report. An AI Agent can assist by pulling the customer’s account profile and recent transaction history to prepare the representative for the conversation.

Fraud claim capture

The representative captures the details of the fraud claim, including the specific transactions disputed, the dates the customer first noticed the unauthorized activity, whether the customer still possesses their card or credentials, whether the customer authorized anyone else to use the account, and any other circumstances relevant to the report. All details are recorded in the fraud claim form.

Claim classification and severity assessment

Based on the claim details, the intake specialist classifies the fraud type — such as card-present fraud, card-not-present fraud, account takeover, ACH unauthorized, or identity theft. The severity is assessed based on the dollar amount, the number of transactions, and whether the fraud is ongoing. An AI Agent may suggest the classification based on the transaction characteristics and flag cases that match high-severity patterns.

Immediate account protection

Based on the fraud type and severity, immediate account protection actions are triggered — such as blocking the compromised card, freezing online access, placing holds on pending suspicious transactions, or issuing replacement credentials. These actions are documented as part of the intake record.

Case creation and routing

The validated and classified fraud claim is created as a formal case and routed to the appropriate investigation team based on fraud type, channel, and severity. The case includes all intake documentation, the customer’s contact information, and any immediate actions taken. The regulatory investigation clock begins from the intake date.

Customer acknowledgment and expectations

The customer receives acknowledgment of their fraud report, information about the investigation process, expected timelines for provisional credit and resolution, and contact information for follow-up. The acknowledgment is documented in the case record.

This process commonly relies on inputs such as the customer’s identity verification, disputed transaction details, account history, and the fraud claim form. It may be triggered by a customer phone call, online report, branch visit, or fraud detection alert requiring customer confirmation. Connected systems often include fraud case management platforms, core banking systems, card management systems, customer authentication tools, and CRM platforms.

Key decision points include whether the customer’s identity is verified through the required authentication protocol, how the fraud claim is classified based on the transaction type, channel, and pattern, what immediate account protection actions are required, and which investigation team should receive the routed case.

Insufficient detail captured at intake, requiring investigators to re-contact the customer and delaying the investigation. Misclassification of the fraud type, routing the case to the wrong investigation team or applying incorrect regulatory timeframes. Account protection actions not triggered at intake, allowing additional unauthorized transactions after the customer reports the fraud. Intake date not captured accurately, creating regulatory compliance risk for investigation and provisional credit timelines. Customer not informed of the process and expected timelines, generating follow-up calls and complaints.

Orchestrates fraud dispute intake from customer contact through case creation and routing across customer service, fraud operations, and the customer in a single workflow.

AI Agents pull account data and transaction history at intake, preparing the representative with context before the customer interaction.

Guides structured claim capture within the workflow to ensure all required details are documented in a single interaction.

Triggers immediate account protection actions based on fraud classification within the workflow, preventing further unauthorized activity.

Routes classified cases to the correct investigation team with complete intake documentation and regulatory timeline tracking.

Preserves the complete intake record including identity verification, claim details, classification, account protection actions, and customer acknowledgment for investigation and regulatory compliance.