Treasury manager

Finance controller

Accounts payable manager

Chief financial officer

Compliance officer

Bank operations lead

This process is used when the organization needs to send a wire transfer and the payment requires formal verification and authorization before execution. It applies when wire amounts exceed automated payment thresholds, when the payee is new or the bank details have changed, when the transfer involves international routing or currency conversion, or when organizational policy requires dual approval for wire disbursements. It is common when treasury, accounts payable, and authorized signatories must coordinate to verify payment details and authorize release. Ideal for financial services, real estate, law firms, professional services, manufacturing, and any organization processing high-value wire payments.

The wire transfer approval process typically involves the payment requestor who initiates the transfer with supporting documentation, accounts payable staff who verify payment details against invoices and purchase orders, treasury operations who validate bank routing information and fund availability, compliance officers who screen for sanctions or fraud indicators, and authorized signatories who provide final approval under dual-control protocols.

Prevented fraudulent transfers through structured verification of payee details, bank routing, and payment authorization before funds leave the account. Accurate payment execution because every wire is validated against supporting documentation such as invoices, contracts, or purchase orders. Dual-control compliance with clear records showing that required approvers authorized the transfer independently. Faster processing for verified transfers by routing standard payments through streamlined approval while flagging exceptions for additional scrutiny. Complete payment audit trail documenting the request, verification steps, approvals, and execution for financial governance and regulatory compliance.

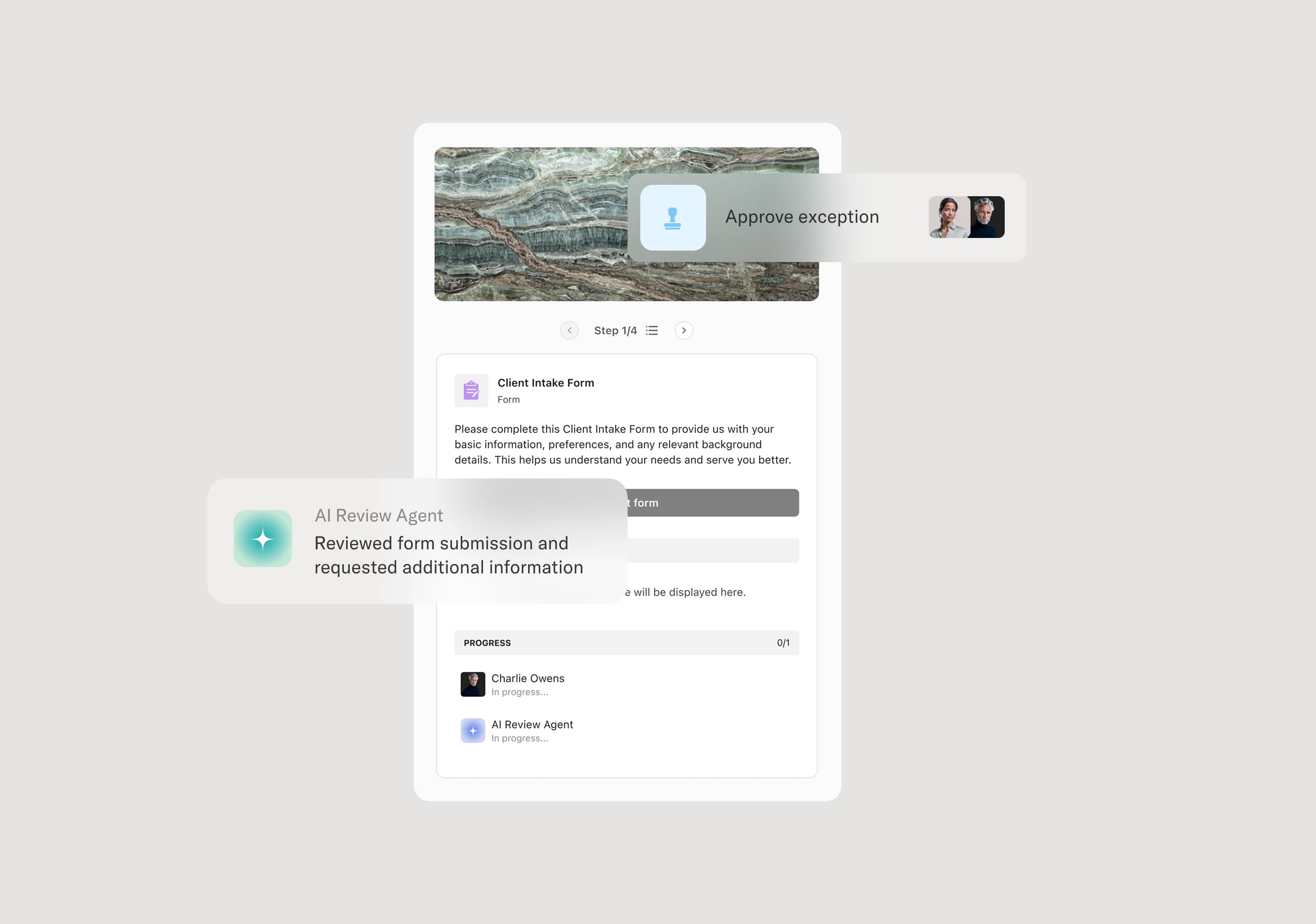

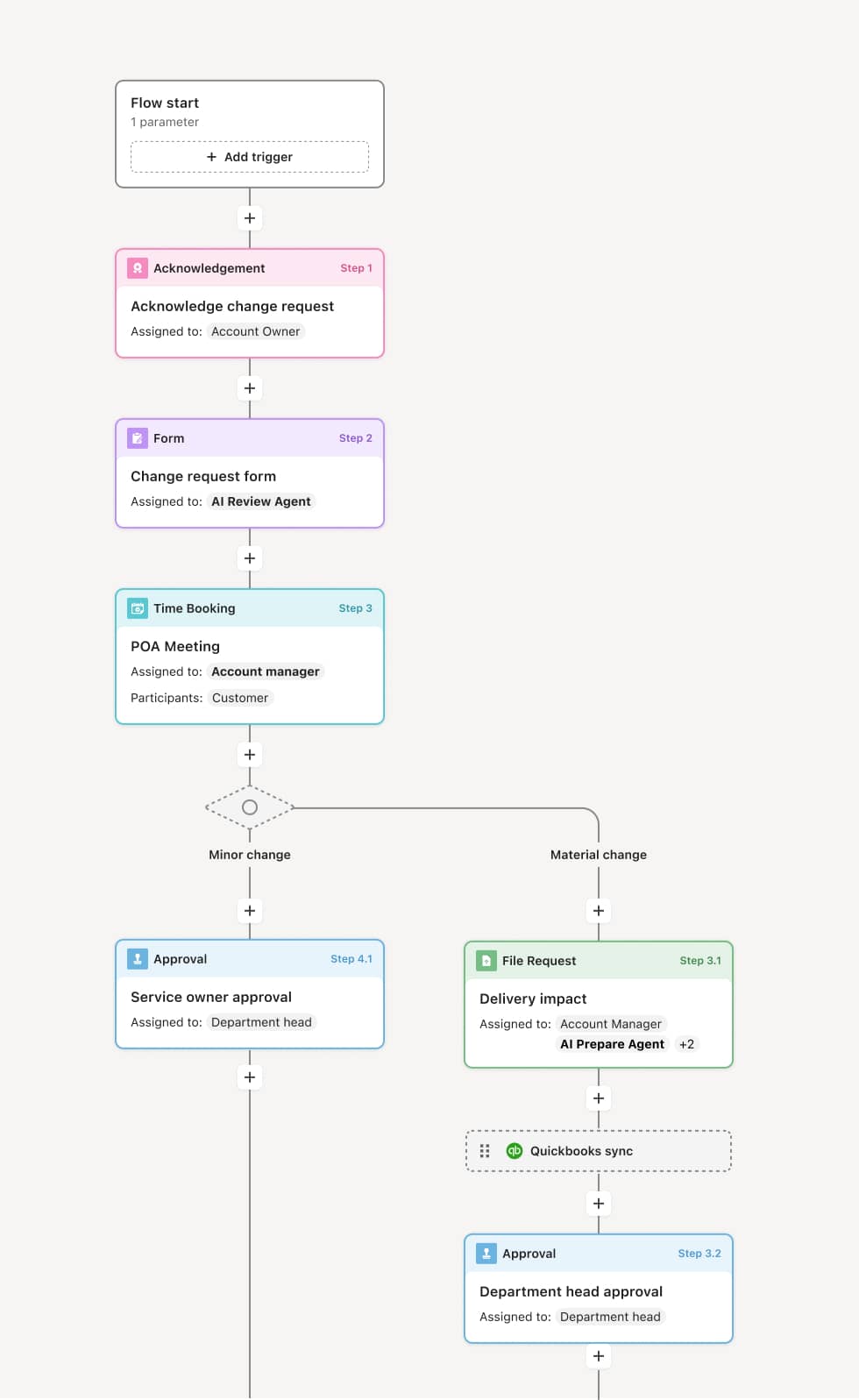

Your version of this process may vary based on roles, systems, data, and approval paths. Moxo’s flow builder can be configured with AI agents, conditional branching, dynamic data references, and sophisticated logic to match how your organization runs this workflow. The steps below illustrate one example.

Transfer request and documentation

The process begins when a payment requestor submits a wire transfer request including the payee name, bank details, amount, currency, purpose, and supporting documentation such as an invoice, contract, or purchase order. An AI Agent can assist by validating the request against known payee records and flagging new payees, changed bank details, or amounts that exceed standard thresholds.

Payment verification

Accounts payable verifies the wire details against the supporting documentation — confirming the amount matches the invoice, the payee is authorized, and the payment has not already been processed. If discrepancies are found, the request is returned for correction before proceeding.

Bank detail and sanctions screening

Treasury operations validates the bank routing information and confirms fund availability. Compliance or treasury screens the payee and routing details against sanctions lists, fraud watchlists, and organizational restrictions. If a flag is raised, the transfer is held for investigation. An AI Agent may cross-reference the payee and routing against prior verified transactions to identify anomalies.

Dual approval authorization

The wire transfer is routed to authorized signatories for approval under the organization’s dual-control policy. Two independent approvers must each review and authorize the transfer. For transfers above defined thresholds, additional senior authorization — such as CFO or treasury director sign-off — may be required. If either approver declines or requests changes, the transfer is returned for revision.

Execution and confirmation

Upon dual approval, the wire is executed through the banking platform. Treasury confirms successful transmission and captures the transaction reference. The requestor and relevant stakeholders are notified of completion.

Record preservation and reconciliation

The complete wire transfer record — including the request, supporting documents, verification steps, approvals, and execution confirmation — is preserved. The payment is reconciled in the general ledger and accounts payable records.

This process commonly relies on inputs such as the wire transfer request, payee bank details, supporting invoices or contracts, fund availability data, and sanctions screening results. It may be triggered by a payment obligation, a vendor request, or a scheduled disbursement. Connected systems often include treasury management systems, banking platforms, ERP systems like NetSuite or SAP for accounts payable and general ledger, and compliance screening tools for sanctions and fraud detection.

Key decision points include whether the wire amount and payee details match the supporting documentation, whether the payee and bank routing pass sanctions and fraud screening, whether the transfer amount triggers escalation to additional approvers, and whether both required signatories independently authorize the release of funds.

Changed bank details not verified through a secondary confirmation channel, creating exposure to payment redirection fraud. Supporting documentation incomplete or mismatched, requiring back-and-forth that delays time-sensitive payments. Dual-control bypass when urgency pressures teams to shortcut the dual-approval requirement. Sanctions screening gaps when new payees or changed routing details are not screened before approval. Reconciliation failures when executed wires are not promptly recorded in the general ledger, creating accounting discrepancies.

Orchestrates wire transfer verification and approval across accounts payable, treasury, compliance, and authorized signatories in a single secure flow.

Enforces dual-control authorization by requiring independent approvals from separate signatories before the transfer can proceed.

AI Agents validate wire requests at submission by checking payee records, flagging changed bank details, and identifying amounts that exceed standard thresholds.

Routes transfers based on amount and risk profile so standard payments are processed efficiently while high-value or flagged transfers receive additional scrutiny.

Connects to treasury, ERP, and compliance screening systems so payment data, fund availability, and sanctions results flow into the approval process.

Preserves the complete wire transfer record including every verification step, approval, and execution confirmation for financial audit and regulatory compliance.